Economic downturns in construction are cyclical and often predictable, but that doesn’t make dealing with them any easier. Mounting financial pressures such as increasing interest rates, volatile material costs, ongoing labor shortages and difficult-to-decipher project pipelines can greatly increase fraud risk.

This post details with construction managers need to know, including:

• the warning signs of financial distress

• the implications for possible fraudulent actions

• how to proactively mitigate risk through internal controls and cultivating ethical best practices

Five Signs of Financial Distress

- Negative Cash Flows

Cash flow is the lifeblood of any organization. Cash inflows need to consistently exceed cash outflows. Shortages in cash will lead to liquidity problems, making it difficult to cover bills and obligations. Managers not only need to often review the company’s cash position as reported in its balance sheet, but also review overall bank account reconciliations to ensure that they are completed in a timely fashion and accurately. - High Debt-to-Equity Ratio

The debt-to-equity ratio is a powerful metric for assessing a company’s debt default risk. It compares a company’s long- and short-term debt to shareholders’ equity (or book value). If this ratio is high, it indicates that the company relies heavily on debt financing, which can be risky during financial distress. - Working Capital Decline

Working capital measures a company’s ability to meet short-term obligations. If accounts payable grow faster than inventory and accounts receivable, working capital may decline and become negative. This situation can signal both financial stress and operational inefficiencies. - Interest Repayments and Debt Pressure

Struggling companies face higher interest rates due to increased risk of loan default. Interest repayments can strain cash flow, affecting profitability. The company’s debt service obligations must be managed effectively to avoid the negative consequences that follow poor debt management. - Excessive deviations from prior construction planning, excluding approved change orders

Discrepancies between project records, invoices and actual work performed that deviate from the original contract must be reviewed and corrected. Deviations may include irregular payment schedules or excessive advance payments not previously approved. Any changes need to be transparent to all related parties to avoid unnecessary delays and resulting negative financial implications.

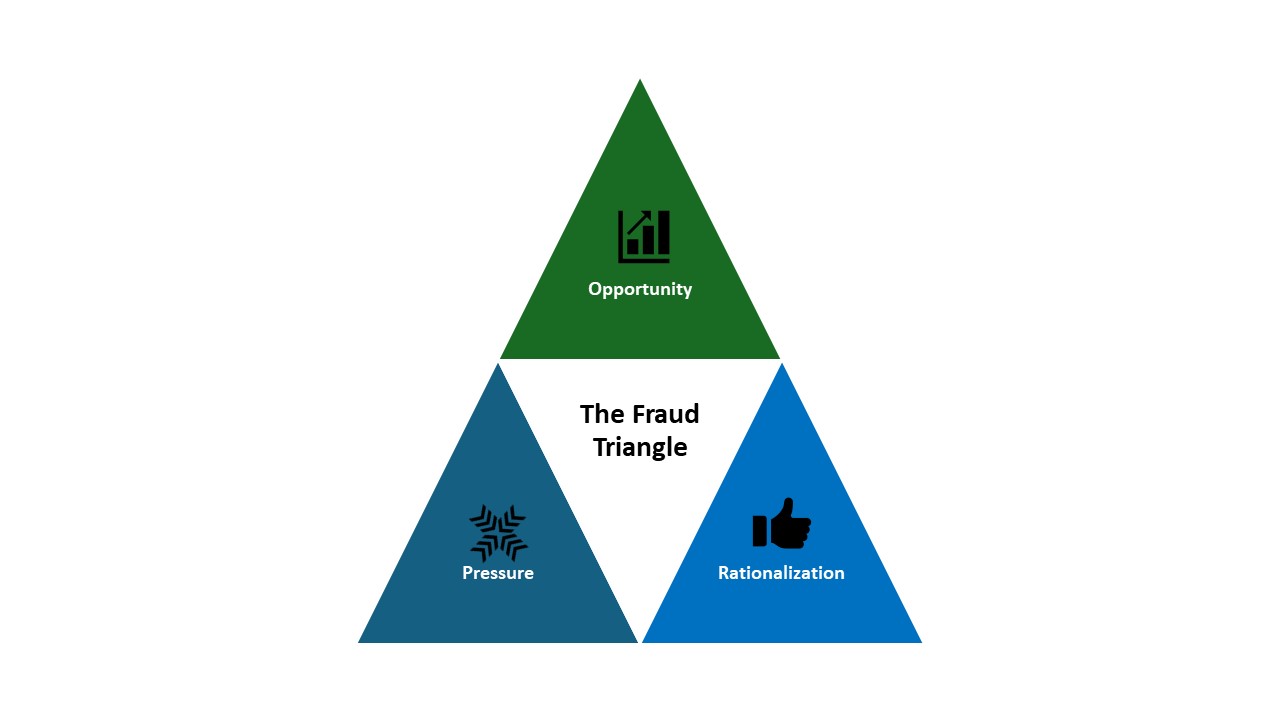

Implications for Fraud Risk and the Fraud Triangle

Implications for Fraud Risk and the Fraud Triangle

While the red flags of financial distress listed above do not guarantee that fraud will occur within a construction firm, it is vital to understand that pressures from an environment of financial difficulty could motivate a person to commit fraud.

Pressure is one of three components of the fraud triangle (see diagram below). The other two components are opportunity and rationalization:

- Opportunity is the ability to exploit a weakness or loophole in the system or organization; this may be manifested as manipulating project documents, invoices or records or colluding with other parties in fraudulent activity.

- Rationalization is the way the fraudster justifies their actions as acceptable or necessary. A contractor may feel motivated to commit fraud due to financial difficulties, market conditions or personal greed. They may rationalize their fraud by thinking that they are entitled to more money, that everyone else is doing it or that they are not harming anyone.

Deception or misrepresentation can occur at any stage of the project, from bidding to completion, and can involve contractors, subcontractors, suppliers, consultants or government officials. Some common examples of construction fraud are:

- Bid-Rigging

Bid-rigging occurs when contractors collude to manipulate the bidding process. Dishonest contractors secretly agree on bid prices, ensuring that one of them wins the contract. This undermines fair competition and inflates project costs. - Falsifying Payment Applications

Contractors may submit inflated payment requests, misrepresenting completed work or materials. These false claims can drain project funds and disrupt cash flow. - Substitution of Materials

Fraudulent substitution involves using subpar or cheaper materials than specified in the contract. This compromises quality, safety and durability. - Ghost Employees and Overbilling

Contractors may create fictitious employees or inflate labor costs. Overbilling for labor hours not worked can siphon funds from the project. - Kickbacks and Bribery

Unethical contractors may receive kickbacks from suppliers or subcontractors in exchange for awarding contracts to these parties. These secret deals harm project transparency.

Effective Mitigation of Fraud Risks

Despite the risks inherent and variety of fraud opportunities in the construction industry, there are actions that can be taken to foster an environment to mitigate these risks proactively. The following internal controls are some examples of front-end fraud risk mitigation:

Segregation of duties: No one person should have complete control over a process or transaction. For example, the person who approves the invoices should not be the same person who pays them, or the person who performs the work should not be the same person who inspects it.

Authorization and approval: All transactions and activities should be authorized and approved by the appropriate level of management. For example, the project manager should approve change orders; the finance manager should approve payments.

- Documentation and record-keeping: All relevant activities should be supported by adequate and accurate documentation and records. For example, the contractor should maintain the contracts, invoices, receipts, timesheets and progress reports for each project.

- Reconciliation and verification: The contractor should periodically compare and verify the information from different sources to ensure its consistency and validity. For example, the contractor should reconcile bank statements with the transactions register and verify invoices with packing slips.

- Monitoring and auditing: The contractor should regularly monitor and audit the performance and compliance of the projects, processes and personnel. For example, the contractor should conduct surprise inspections, review financial statements or hire external auditors.

Internal controls alone are not enough to prevent construction fraud. Contractors should also create a strong ethical culture that discourages fraud and encourages reporting. Some of the ways to create a strong ethical culture are:

- Tone at the top: Senior management should set an example of honesty, integrity and accountability for the rest of the organization. They should communicate and enforce the code of ethics, anti-fraud and whistleblower policies.

- Training and education: The contractor should provide regular training and education to employees and stakeholders on the signs and consequences of fraud; roles and responsibilities and reporting channels and procedures.

- Incentives and rewards: The contractor should provide positive incentives and rewards for the employees and stakeholders who demonstrate ethical behavior, achieve stated objectives or report fraud. They should also avoid negative incentives and pressures that may tempt employees to commit fraud.

- Reporting and feedback: The contractor should establish and maintain effective reporting and feedback mechanisms that allow employees and stakeholders to report fraud or raise concerns without fear of retaliation. They should also investigate and respond to any reports of potentially fraudulent activity promptly and appropriately.

An Ounce of Prevention Goes a Long Way

Construction managers need to do more than simply recognize the risk presented by financial distress in terms of fraudulent activity – they need to take a proactive approach to mitigate the risk. Utilization of robust internal controls needs to be coupled with an ethical culture that continually promotes transparency, training and two-way communication. These actions will help foster an environment that promotes ethical behavior and emphasizes accountability, ultimately reducing opportunities for fraudulent activities.

For more information on proactive risk management in times of financial distress, contact Sam Haagenson or submit a query to Vertex.

The Author

Charles Lewing

CFE

Senior Consultant, Technical Claims & Disputes

Charles Lewing brings a wealth of diverse finance and administration experience, notably as a Senior Consultant at Vertex.