Construction projects are prone to delays resulting from loss events during construction with consequences for all parties. For contractors, delays can result in extended general conditions costs and other delay damages. For owners, delays to commercial operations can mean loss of income. The insurance industry writes policies which insure against delay risks stemming from covered events in the form of Builder’s Risk policies and Delay in Start-Up (DSU) products aimed at contractors and owners respectively.

These types of policies are designed to mitigate the financial risk associated with the impact of a loss event and typically provide coverage for:

- Repair and mitigation expenses related to a loss event.

- Extra expenses incurred to maintain the scheduled progress.

- Loss of income.

When an insurance claim is submitted, the impact of the loss event on the completion of the project needs to be determined to calculate the financial loss suffered. Given how common delays are on construction projects, an extensive body of knowledge exists on how to measure delay. Still, while a wealth of information is available on delay analysis, there is limited literature that specifically focuses on delay analysis in the context of Builder’s Risk and DSU insurance.

This article addresses this knowledge gap by outlining considerations and approaches for measuring the impact of delay in Builder’s Risk and DSU insurance claims.

The Evolution of Builder’s Risk and Delay in Start-Up Insurance

Before considering how delays covered by these types of policies should be measured it is necessary to understand the mechanics of Builder’s Risk / DSU insurance coverage, which was done by studying typical policy language and a review of the limited literature available on the analysis of delay in Builder’s Risk and DSU insurance claims.

Construction projects are exposed to a myriad of risks: fire, theft, water damage, and accidents. Builder’s risk insurance originated in the late 19th century as a hybrid policy that combined aspects of property insurance with inland marine coverage to offer risk mitigation of certain unforeseen loss events to the contractor. Over the years, it has evolved into Builder’s Risk insurance as we know it today.[1]

The origin of Delay in Start-Up (DSU) insurance, sometimes referred to as Advance Loss of Profits (ALOP) insurance, is difficult to trace. It appears that this type of insurance started in the early 1980s and first emerged as a topic at the IMAI Insurance Conference in 1982 in Montreux.[2] Other sources also reference the emergence of DSU Insurance policies in the 1980’s.[3]

Expert Sources Offer Guidance from the Insurance Industry Perspective

Some degree of guidance on Builder’s Risk and DSU insurance claims comes from within the insurance industry.

The world’s second largest reinsurer, Swiss Reinsurance Company Ltd, commonly known as Swiss Re, released a technical publication in 2003 to assist underwriters and the parties involved in large construction projects with information on the fundamentals for Builder’s Risk and DSU insurance claims.[4] This comprehensive brochure provides information on periods and dates, progress monitoring, risk evaluation, claim handling, and typical problem areas. The brochure does not directly discuss methods of delay analysis but provides useful information on how the overlap of insured and un-insured delays should be dealt with.

In 2012, IMIA and LEG collectively produced a practice note on Delay in Start Up Insurance.[5] The International Association of Engineering Insurers (originally set up under the designation of “International Machinery Insurers’ Association, which led to its moniker of “IMIA”) is a network of experts in engineering insurance from around the world that acts as a discussion forum and produces papers on topics of engineering insurance.[6] London Engineering Group (LEG), a consultative body for insurers of engineering class risks produces various industry recognized papers, coverage clauses, and guidance notes. Membership is drawn from the various insurance and re-insurance companies actively involved in underwriting risks within the engineering classes.[7] IMIA and LEG’s two-page practice note generally deals with insurance-related matters like coverage, indemnity, and deductibles, but does not discuss methods for determining delay to completion as a result of a loss event.

A 2017 article from the international law firm Simmons & Simmons published on the Lexology website (the most comprehensive source of international legal updates, analysis, and insights) titled “Delay in Start Up insurance and Delay Analysis Technique” does review the common construction delay analysis methods when applied in DSU claims.[8] The article considers DSU policy wording in its evaluation of common construction delay analysis methods to determine the most suitable delay analysis method. When comparing common methods, such as As-Planned vs. As-Built, Impacted As-Planned, As-Planned But-for, Collapsed As-Built, and Windows Analysis, the author of the article favors the Collapsed As-Built and Windows Analysis methods.

Influence of Policy Terms on Delay Analysis

Policies typically include two specific terms directly relating to the delay caused by the loss event: Period of Restoration and Period of Delay. It is important to distinguish between these two terms.

Period of Restoration:

Wording may vary but the Period of Restoration is commonly defined as the period required to execute repairs as a result of the loss event. It starts immediately after the loss event and ends when all repairs related to the loss event are completed.

Period of Delay:

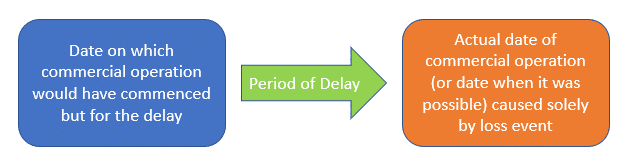

The Period of Delay (Fig. 1 below) is in essence the actual delay to project completion because of the loss event. The starting point of the period of delay is the date when commercial operation would have commenced if the loss event did not occur and ends with the actual commencement of commercial operation.

Figure 1. Period of Delay

In many cases, a loss event and resulting Period of Restoration causes a delay to both completion and the start of commercial operation. The duration of the Period of Restoration is dependent on the time required to complete all repair activities. This is not necessarily the same as the Period of Delay, which is determined by the impact on the critical path and overall completion of the project (or subset of the project that would have been available for commercial use). The critical path is the longest sequence of work activities which establishes the minimal overall duration to project completion (or another milestone). If the duration of critical path activities is extended, completion will be delayed. The slippage of the completion date caused by the loss event represents the Period of Delay.

The relationship between the two terms can be further explained by looking at the delay analysis concept of cause and effect. The loss event and the subsequent restoration (the cause) impact the planned execution of the project activities and might delay the completion of the project (the effect). If the Period of Restoration drives the critical path to planned completion, it will delay the start of commercial operation, resulting in delay damages.

Complexities that Impact Delay Analysis in Builder’s Risk and Delay in Start-Up Insurance Claims

The occurrence of a loss event has several consequences that influence the execution of a construction project. When a loss occurs, completing repairs expeditiously is typically a priority to mitigate the impact on the planned completion of the project. The original construction approach and sequencing of work depicted in the pre-loss schedule no longer properly models the work, because new repair and restoration activities are introduced. This may result in resequencing or acceleration of activities to mitigate the impact of the loss event. The pre-loss schedule is typically updated or replaced by a new schedule that incorporates the repair and mitigation activities. Based on these changes, the critical path in the pre-loss schedule and the mitigation schedule may differ and activities that were critical in the pre-loss schedule may no longer be critical in the mitigation schedule, as they are overcome by “more critical” activities associated with the loss event. Further, during the Period of Repair, other delays may occur that result in concurrent delays to completion.

Best Practices in the Delay Analysis Process

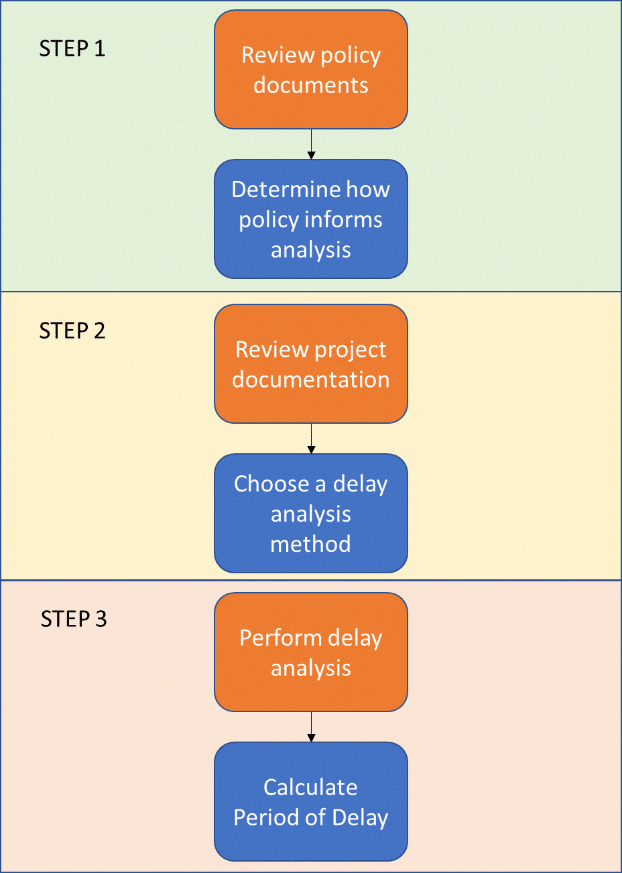

Given the complexities involved in these types of claims a structured analysis approached is recommended. The following steps (Fig. 2 below) establish a process for analyzing the delay and ultimately determining the Period of Delay resulting from the loss event:

Figure 2. Builder’s Risk and DSU delay analysis process

Step 1 – Review of Policy Documents

The first step is to review the insurance policy, to determine if a methodology is specified. It is very likely that the policy will not directly prescribe a specific analysis method.

If no method is prescribed, the policy language might provide some guidance on the most suitable method to utilize. Policies would typically describe coverage by noting that the insured will be indemnified for the cost associated with the loss event and the loss of earnings that would have been derived from the project but for the delay. The phrase “but for the delay” in an insuring clause may be language that supports the use of a Collapsed As-Built analysis, also known as a “but for” method.

In addition to the method of analysis, the policy review should also consider the implication of policy terms like Basis of Indemnity, Date of Completion, Period of Delay, Period of Restoration, and other terms that may influence the measurement of delay. The review should also determine whether the policy indicates how concurrent insured and uninsured delays should be dealt with, such an when the loss event repairs take place at the same time or overlap with another delay that is not associated with the loss event or covered by the policy.

Step 2 – Choose a Delay Analysis Method

Several factors can influence the choice of a delay analysis method. The Association of the Advancement of Cost Engineering International (AACE) published Recommend Practice 29R-03 “Forensic Schedule Analysis” in 2011, which references various methods of delay analysis.[9] This Recommended Practice is commonly used for forensic schedule analysis guidance in the United States. There are numerous methodologies available that AACE divides into Method Implementation Protocols (MIP), which are categorized as MIP 3.1 through MIP 3.9 (Fig. 3).

Figure 3. AACE RP 29R-03 “Taxonomy of Forensic Schedule Analysis”

While AACE Recommended Practice 29R-03 may be used internationally, other references, such as the Society of Construction Law (“SCL”) Delay and Disruption Protocol are commonly used internationally.

Both AACE and SCL recognize that there is no “one-size-fits-all” method for delay analysis and that multiple factors should be considered when selecting a methodology, summarized in Table 1 below:

Factors to be considered in selecting a Delay Analysis Method

| AACE Recommended Practice 29R-03 | SCL Delay and Disruption Protocol |

| Contractual requirements Purpose of analysis Source data: availability and reliability Size of the dispute Complexity of the dispute Budget for forensic analysis Time allowed for analysis Expertise of the Analyst and resources available Forum for resolution Legal or procedural requirements History of methods not accepted | The relevant conditions of the contract The nature of the causative events The nature of the project The value of the dispute The time available The nature, extent, and quality of the records available The nature, extent, and quality of the schedule information available The forum in which the assessment is being made |

Table 1. Factors in selecting Delay Analysis Method – AACE and SCL

Perhaps the most significant of these factors is the availability of the relevant information (source data and records). The information available should be reviewed to determine which of the industry’s recognized delay analysis methods can be applied. The basic requirements to execute a specific delay analysis method are summarized in Table 2 below:

Delay Analysis Methods – Basic Requirements

| Baseline Schedule | Restoration Activity Information | Updated Schedules | As-Built Schedule | |

| As-Planned vs As-Built | ✓ | ✓ | ||

| Impacted As-Planned | ✓ | ✓ | ||

| Window Analysis | ✓ | ✓ | ||

| Collapsed As-Built | ✓ | ✓ | ||

| Time Impact Analysis | ✓ | ✓ | ✓ |

Table 2. Delay Analysis Method Basic Requirements

If the policy covers the insured for the loss of income that would have been earned “but for” the delay, the Collapsed As-Built method may be the most appropriate method based on similar language found in the description of subtractive modeling methods in the AACE Recommended Practice (“… the subtractive modeling methods are one of the only tools to identify and quantify the overall extent to which the contractor’s actual performance would have resulted in a project duration shorter than the baseline schedule, but for the delays.”) To successfully apply the Collapsed As-Built method, the following information is utilized:

- An accurate logic-linked As-Built Schedule

- Detailed information on Restoration Activities

The selection of a delay analysis method to perform the analysis depends on the review of the policy documents, understanding of available data and various other factors. Each delay analysis typically has its pros and cons. Examples of these methodologies and their strengths and weaknesses can be found in Vertex’s article on Understanding Construction Scheduling – A Critical Path to Successful Claim Handling.

Step 3 – Perform the Analysis

The main objective of delay analysis in Builder’s Risk and DSU insurance claims is to determine the Period of Delay that resulted from the occurrence of the loss event. Again, the Period of Delay is the time between the dates when commercial operation would have commenced but for the delay and the actual date of the commencement of commercial operation. While the actual date of commencement of commercial operation should not be difficult to determine, it may have been influenced by other delays unrelated to the loss, which must also be considered. The date when commercial operation would have commenced if the loss event did not occur may be established from schedule data prior to the loss event, or through subtractive modeling analyses such as the Collapsed As-Built method.

For example, the following is a high-level summary of the steps required to execute the Collapsed As-Built analysis:

- Remove the restoration activities and the effect of the restoration activities on related activities from the logic-linked As-Built Schedule.

- Identify concurrent delays and pacing delays.

- Eliminate the impact of concurrent delays and pacing.

- Re-calculate the completion date.

If executed correctly, the re-calculated completion date of the collapsed schedule would constitute the date when commercial operation would have commenced if the loss event did not occur. To ensure accurate results, it is critical that concurrent delays and pacing be correctly considered.

- Concurrent delays in this context refer to the simultaneous occurrence or the overlap of insured delays and uninsured delays. To address concurrency, the policy should be consulted to determine whether any guidance on how to treat concurrent delays is provided. If not, guidance may be found in insurance industry and construction industry literature.

- Pacing occurs when the contractor decides to slow the progress of other activities taking place at the same time as the delay created by the loss event. This happens very often in Builder’s Risk and DSU Insurance claims, especially when the loss event is of such significance that it will likely delay project completion. In this scenario, the loss event repairs will be critical. The contractor may choose to focus its efforts on the loss event repair activities and not on other activities that will no longer dictate the completion date. Each identified pacing delay should be considered to determine whether sufficient resources could have been utilized to complete the activity within its planned duration if it was required. If it is realistically possible to do so, the effect of the pacing delay should be removed from the collapsed schedule.

A challenge to implementing a collapsed- as-built analysis is that a logic-linked As-Built Schedule is very seldom available, and would need to be generated by the delay analyst. If a logic-linked As-Built Schedule is not available, logic may be introduced to the As-Built Schedule; however, this can be a very complex, time-consuming, and costly process. A further disadvantage to this approach is that the updated As-Built Schedule may be subject to criticism for analyst decisions used to establish the logic. Because of these challenges, one or more of the other delay analysis methods may be a better choice for determining when the project would have been completed but for the loss event, such as the Windows Analysis method, which allows for the evaluation of critical and near-critical paths.

The final step in the process to determine the Period of Delay is to measure the time between the date when the project would have been completed exclusively of the loss event and the actual date of project completion.

Common Frameworks for Delay Analysis Serve Both Parties When Claims Arise

Although the objective of delay analysis in Builder’s Risk and DSU Insurance claims and construction contract claims is the same, there are some noteworthy differences. Where the construction agreement influences the analysis in construction contract claims, the insurance policy fills this role in Builder’s Risk and DSU Insurance claims. Since insurance policies often do not dictate how the delay analysis is to be performed, the extensive body of knowledge on delay analysis developed for construction contract claims can be successfully applied in the context of these claims. In our experience, the Collapsed As-Built method is one technique that seems to align most closely with insurance policy language – provided that the proper steps are followed and analysis is carefully performed – but that other methodologies, such as a Windows Analysis, are appropriate for the analysis of these types of delay impacts.

For more information on delay analysis in Builder’s Risk and Delay in Start-Up insurance claims, please contact Jeff Katz at jkatz@vertexeng.com.

Article Written By:

Dr. Hendrik Prinsloo, Pr. CPM, BSc, MSC, CEO of HPM Consultants

Jeffrey Katz, PE, PSP, Executive Vice President of The Vertex Companies LLC

References:

[1] https://buildersrisk.net/understanding-builders-risk-insurance-ebook/#dos

[2] https://www.imia.com/wp-content/uploads/2013/05/New-Development-in-Advance- Loss-of-Profits-Insurance-WGP-06_53-96.pdf

[3] https://www.jlta.com.au/docs/Construction_Whitepaper_201306.pdf?201507190539

[4] https://www.swissre.com/dam/jcr:b76d1bbf-2d0b-47f1-911a-509232761aaf/pub_delay_in_startup_insurance_en.pdf

[5] https://www.imia.com/wp-content/uploads/2013/10/LEG-DSU-An-Overview-1358955726.pdf

[6] https://www.imia.com/about-imia/

[7] https://www.londonengineeringgroup.com/resource-library

[8] https://www.lexology.com/library/detail.aspx?g=814a2f33-9e51-4a0d-8e9e-432c550c8940

[9] AACE International Recommended Practice No. 29R-03, Forensic Schedule Analysis, Rev. April 25,2011.

The Author

Jeff Katz

PE, PSP, CCM, CCA

Senior Managing Director, Commercial Damages & Investigation

Jeff Katz is a Senior Managing Director of Vertex who leads Vertex’s contract claims practice. Mr. Katz is a professional engineer who has been retained as an expert or consultant on large files across North America.