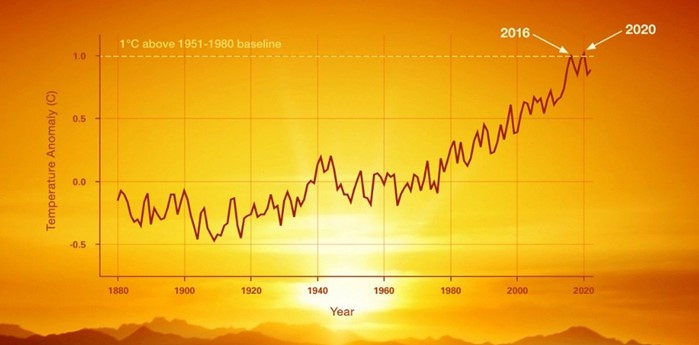

Climate change is a long-term shift in weather patterns and temperatures. Although the Earth is naturally in a warming cycle, human activities since the Industrial Revolution have accelerated the heating of the planet. Over the last 250 years, human activity has increased the Earth’s temperature (Figure 1) by 2.0° Fahrenheit, while ocean temperatures have risen almost 2.0° and sea levels have risen 8-10”. The rate of increase in ocean temperatures and sea levels has also accelerated in the last 50 years.

The direct causes of climate change include:

- burning of fossil fuels

- increased agricultural activities

- deforestation

Figure. 1 Global average temperature (degrees Celsius) change since 1880, Source: nps.gov

For claims and underwriting professionals, the realities of these environmental changes represent unique challenges to managing and mitigating risk. In this post, we:

- Discuss the categories of risk associated with climate change

- Provide insight into the rising cost of climate-related claims

- Examine the very tangible effects of climate change on weather events

- Explore new technologies for reducing the impact of climate change and the associated risks

- Provide recommendations for innovative ways that claims and underwriting professionals can proactively assess risk associated with climate change

Climate-Related Risks: A Multi-Dimensional Problem

Climate-related risks include three separate segments:

- Physical Risk: the risk of actual physical damages incurred during severe weather events

- Transition Risk: the potential abrupt transition to a low-carbon economy causes investments to lose value

- Liability Risk: the risk of being sued for one’s role in creating climate change. Liability risk is an emerging risk that could challenge law statutes.

The Impact of Climate Change on Claims and Underwriting

Due to climate change and its effects on weather events, billion-dollar claims have increased in frequency:

- In the 1980’s, there were an average of 3.4 billion-dollar claims (inflation adjusted) per year.

- In the 2010s, there were an average of 13 billion-dollar claims per year. These billion-dollar claims include damages sought due to the impact of droughts, wildfires, hailstorms, floods, tropical cyclones, winter storms and deep freezes.

- In 2024, an all-time high of 27 billion-dollar claims were filed in the United States. Hurricanes Helene and Milton caused $59.6B and $25B, respectively.

Understanding how and why this trend is likely to continue requires a closer look at the specific ways in which climate change dramatically increases the scale of these costly disasters, making seven-figure claims typical.

With Climate Change Comes Severe Weather Events and Greater Risk

As the Earth’s temperature rises, changes in climate patterns have significant impact on the frequency and severity of weather events. As these disasters strike, claims and underwriting professionals find their jobs significantly more challenging, especially as historical risks are no longer predictive of future risks.

Extreme Heat/Wildfires

In the United States, a significant portion of the West has seen a 2-4” annual reduction in rainfall. The warmer, drier conditions have led to a rapid increase in wildfire acreage burned per year. Available data indicates that there has been a 200% increase in wildfires in the US since 1990. Wildfires destroy significant amounts of infrastructure and can lead to future mudslides when rain does arrive in the scarred area. Wildfires can also create pollution events, impacting sites with Combustion Byproducts (CBP) or damaging tanks that store hazardous chemicals. VERTEX has nationwide support staff to quickly mobilize to CBP-impacted property and has extensive experience managing wildfire claims.

Tropical Cyclones

Tropical cyclones (called hurricanes in the U.S.) are fueled by warm ocean waters. As the world’s ocean temperatures rise, the ability for tropical cyclones to form increases. Research indicates that the frequency of Category 3 or higher (considered major hurricanes) has doubled since 1980. Compounding the risk, the states currently experiencing the greatest increase in population in the U.S are Florida, Texas and the Carolinas — are all in hurricane-prone areas. Hurricanes damage property with both wind impacts and more significantly, storm surge. Claims arising from hurricanes include roof damage, water intrusion, and mold events.

Excessive Rain/Flooding

Increased air and water temperature lead to more moisture in the atmosphere, resulting in upticks in precipitation. While the western U.S. has become drier, the opposite has been true in the eastern half of the country. The eastern U.S. has seen an increase of 2-4” of annual rain over the last 40 years. According to current research, 100-year rain events are becoming more frequent, potentially every few decades in some areas. These extreme rain events lead to property and pollution events, including water intrusion, mold, sewage overflows, sedimentation and landslides/mudslides.

Extreme Cold

Although climate change is typically associated with increased global temperatures, extreme weather phenomenon can also lead to extreme cold events. In January 2025, cities such as New Orleans, LA, Pensacola, FL, and Myrtle Beach, SC saw their first snowfall in decades. In February 2021 Winter Storm Uri pushed extreme cold weather as far south as South Texas, crippling the state for weeks. Uri brought the coldest air into several cities in Texas in over 100 years, and at one point every county in Texas was under a Winter Storm Warning. Uri caused severe power outages and water pipe ruptures in almost every area of the state. Claims arising from Uri included significant water damage and mold events. Due to the widespread power and travel issues, these claims were exacerbated by slow emergency response times. The total damages claimed due to the effects of Uri approached $195B.

Tornadoes

Due to climate change, Tornado Alley has been shifting eastward over the last 30 to 40 years. Climatologists have theorized that the warmer Gulf of Mexico has shifted wind patterns and moved the U.S “dry line” to the east. Tornado frequency trends indicate that fewer tornadoes are occurring in Oklahoma and Texas, while frequency has increased in Eastern Arkansas, Southeast Missouri, western Tennessee and northern Mississippi and Alabama. This trend has pushed higher the odds of a tornado striking the metropolitan areas of Little Rock, Memphis and Nashville. Tornadoes (and severe thunderstorms) can lead to hail damage, wind damage and flash flooding. Additionally, if tornadoes hit residential or commercial areas, they can cause significant property damage and pollution events from storage tank ruptures, truck rollovers and/or train derailments.

Another Toll Bad Weather Takes: Infrastructure Strain

Along with severe weather events, climate change puts a significant strain on infrastructure across the world. Due to budget constraints, maintenance and upgrades on infrastructure including the electrical grid, bridges and roads and water supply systems has been deferred. When severe weather events occur, this infrastructure is now “behind the times” and cannot keep up with expected performance during these events. This exacerbates the issue, as power outages take longer to repair, bridges may fail during severe floods and water supply systems are more severely impaired during heavy rain events. Infrastructure strains have also been worsened by the migration of U.S. population to coastal areas in the last decade, leading to increased impervious areas that lead to more severe flooding.

Architectural experts estimate that over 2.5 trillion square feet worldwide will be either constructed or renovated in cities in the next 35 years, which is the equivalent of another New York City every 35 days. This rapid development/renovation will lead to even further strains on the infrastructure system.

New Ideas to Reduce the Impact of Climate Change: Good but Not Necessarily Risk Free

The drive to reduce the impact of climate change has created new technologies that can reduce carbon consumption or remediate carbon output. While effective, the advances come with risks of their own.

Renewable Energy

In the past 20+ years, renewable energy sources have skyrocketed in the U.S. Renewable energy sources include wind turbine power, solar power, tidal power and electric vehicles. Renewable energy sources now account for 8-9% of the U.S energy production. Although renewable energy is reducing carbon consumption, these sources come with their own risks.

- Wind turbines can be damaged by severe thunderstorms, hail, and tornadoes. These storms can damage the turbine itself or topple them, leading to hydraulic oil and diesel fuel releases.

- Solar panels installed on residential/commercial properties can cause water intrusion events by either improper installation, lack of maintenance or severe weather events. These water intrusion events damage property and can lead to mold growth events. Solar farms (large scale solar panel sites) can be impacted by severe rainfall/storm events. These events can destroy the panels and lead to landslides, creating sedimentation events and ecological damage.

- Electric vehicles utilize lithium batteries as a power source. These vehicles reduce petroleum dependence, but also present property and environmental risks. Lithium batteries can ignite due to manufacturing impurities, improper installation, physical damage or overcharging. Lithium fires can lead to the destruction of the car and residential properties if not extinguished in time. Additionally, lithium battery warehouses can be lost due to a fire at the facility. These lead to large loss claims due to property damage and significant environmental impacts.

Carbon Sequestration

Carbon sequestration is a new technology that involves the capturing of carbon dioxide and injecting it back into the earth. This technology requires significant infrastructure, including capturing facilities, pipelines and injection wells. As with the renewable energy sources, this technology comes with risks. Pipelines can be damaged or leak, injection wells can leak or have a blowout and injection events can lead to seismic events.

Innovative Ideas for Lowering the Risks Driven by Climate Change

No one doubts the challenges that claims and underwriting professionals face when dealing with climate-related risk. With challenge, however, comes opportunity for unique underwriting processes and products.

Several innovative ideas can be utilized to lower the climate-related risk for insurance providers:

- Evaluating operating procedures and performing compliance surveys and/or audits can detect inherent risks in a business.

- A significant risk associated with climate change is that former weather pattern data may not be relevant or useful anymore; utilizing artificial intelligence (AI) to review recent data for rainfall/wind/extreme temperatures can properly assess risk to a property.

- Underwriters can integrate environmental, social and governance (ESG) factors into their risk assessments. ESG factors include carbon emissions reduction, business operations and logistics review and developing a sustainable energy strategy.

The Vertex Companies, LLC (VERTEX), with an experienced staff of professional engineers, professional geologists, and environmental scientists, can assist underwriters and claim handers on climate impact risks and claims. VERTEX has personnel across the country and can quickly get resources on the ground following climate related claims such as CBP, mold events, structural damage, and other pollution events. For more information, please contact Michael Bator at mbator@vertexeng.com.

The Author

Michael Bator

PG

Senior Managing Director, Claims, Disputes and Forensics

Michael Bator is a Senior Managing Director of Environmental Insurance at VERTEX with over 22 years of experience in the environmental consulting industry. In this position, Mr. Bator is responsible for claim investigations, invoice and proposal reviews, and environmental site assessments.